Below are some research articles by authors working for the public sector that we say are concerned with what we call Asset Class Dynamics, and which use the same kind of data that FlowPro offers, especially the Asset Class Dynamics / Country Dynamics data, but also in some instances Fund data.

We open with a generally useful guide paper. Then the next set of papers are more specifically concerned with the Investors. Finally, we mention other more general papers.

Guide

Capital flow data—A guide for empirical analysis and real-time tracking

This paper provides an analytical overview of the most widely used capital flow datasets. The paper is written as a guide for academics who embark on empirical research projects and for policymakers who need timely information on capital flow developments to inform their decisions. We address common misconceptions about capital flow data and discuss differences between high-frequency proxies for portfolio flows. In a nowcasting “horse race” we show that high-frequency proxies have significant predictive content for portfolio flows from the balance of payments (BoP). We also construct a new dataset for academic use, consisting of monthly portfolio flows broadly consistent with BoP data.

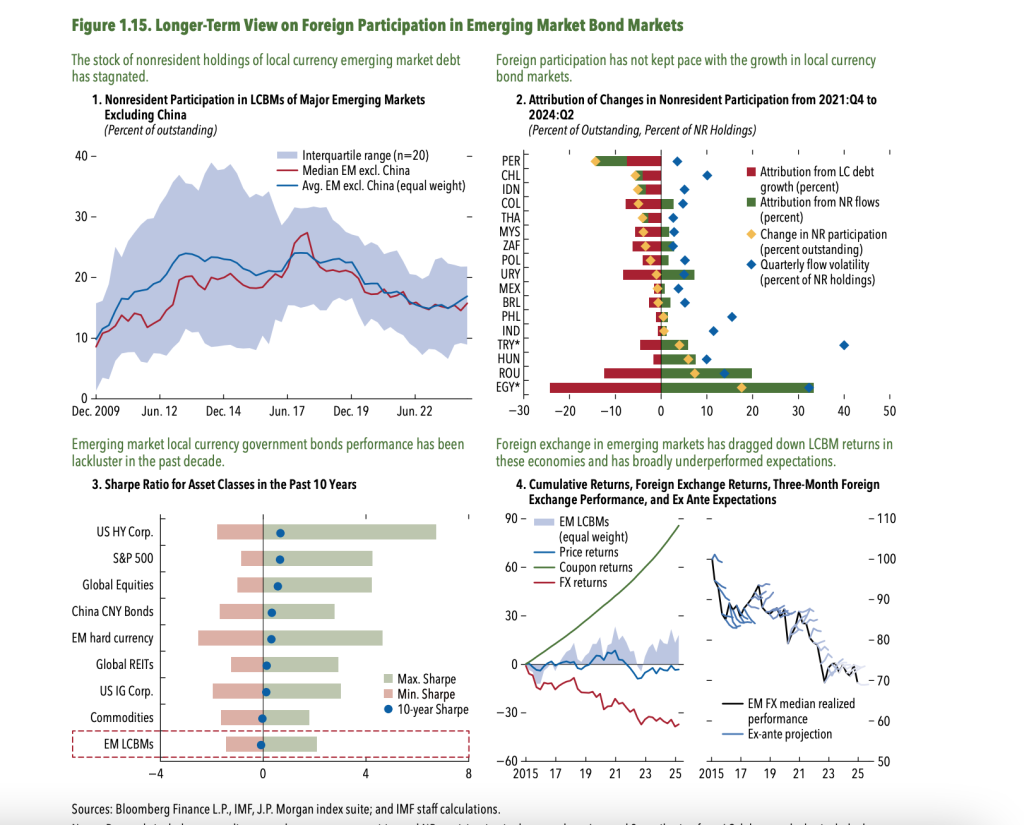

Emerging markets have endured a long period of tepid portfolio flows. A prolonged period of weak emerging market currencies in which the dollar has strengthened in both good and bad states of the world, along with increased volatility in foreign exchange markets, has made the asset class less appealing. Additionally, following a period of strong interest from foreign investors in the years after the global financial crisis, nonresident interest in local currency bond markets (LCBMs) in emerging markets has stagnated. Since 2018, nonresident participation in LCBMs has declined (Figure 1.15, panel 1), which can be attributed to foreign investors having not kept up with the growing size of these markets (Figure 1.15, panel 2). Although the growing support from domestic institutional investors has bolstered recent fiscal expansion and somewhat mitigated recent spillovers from the external environment for some major emerging markets, the declining nonresident interest could pose challenges for weaker emerging markets that lack the necessary domestic buffers. This weakness of foreign flows into emerging market LCBMs may in part be the result of underwhelming performance of the asset class over the past decade. With lackluster 10-year cumulative returns but high realized volatility compared with that of other fixed-income assets such as US corporate bonds (Figure 1.15, panel 3), the Sharpe ratio for LCBMs has been among the lowest compared with those of liquid assets. Weak LCBM performance has primarily been driven by weak emerging market currencies, which have appreciated against the dollar in only 2 out of the past 10 years (Figure 1.15, panel 4). Realized emerging market currency performance continues to underwhelm ex ante expectations, based on surveys of analysts.

Who Holds Sovereign Debt and Why It Matters

This paper studies whether investor composition affects the sovereign debt market. We construct a data set of sovereign debt holdings by foreign and domestic bank, nonbank private and official investors for 101 countries across three decades. Compared with other investors, private nonbank investors absorb a disproportionate share of the debt supply, and their demand for emerging market debt is most price responsive. A counterfactual analysis of emerging market sovereigns shows a 10% increase in debt leads to a 5.8% yield increase but an outsized 8.4% increase without nonbank investors. We conclude that sovereigns are vulnerable to the loss of nonbanks.

Benchmark-Driven Investments in Emerging Market Bond Markets: Taking Stock

This paper reviews the role of benchmark-driven investments in EM local bond markets. We provide an overview of how key EM bond benchmark indices are constructed, how they affect the behavior of investment funds, and what are the likely implications for capital flows and policy-making. Several methods are presented suggesting that the amount of assets benchmarked against widely followed EM local-currency bond indices have risen fivefold since the mid-2000s to around $300 billion. Our review suggests that the benefits of index membership may be tempered by portfolio outflow risks for some countries. This is because benchmark-driven investments may increase the importance of external factors at the expense of domestic factors, raising the risks of outflows unrelated to recipient country fundamentals. Some countries may be disproportionately exposed to these risks, reflecting the way the indices are constructed.

Serkan Arslanalp, Dimitris Drakopoulos, Rohit Goel & Robin Koepke

Tracking Global Demand for Emerging Market Sovereign Debt

This paper proposes an approach to track US$1 trillion of emerging market government debt held by foreign investors in local and hard currency, based on a similar approach that was used for advanced economies (Arslanalp and Tsuda, 2012). The estimates are constructed on a quarterly basis from 2004 to mid-2013 and are available along with the paper in an online dataset. We estimate that about half a trillion dollars of foreign flows went into emerging market government debt during 2010–12, mostly coming from foreign asset managers. Foreign central bank holdings have risen as well, but remain concentrated in a few countries: Brazil, China, Indonesia, Poland, Malaysia, Mexico, and South Africa. We also find that foreign investor flows to emerging markets were less differentiated during 2010–12 against the background of near-zero interest rates in advanced economies. The paper extends some of the indicators proposed in our earlier paper to show how the investor base data can be used to assess countries’ sensitivity to external funding shocks and to track foreign investors’ exposures to different markets within a global benchmark portfolio.

Emerging Market Portfolio Flows: The Role of Benchmark-Driven Investors

Portfolio flows to emerging markets (EMs) tend to be correlated. A possible explanation is the role global benchmarks play in allocating capital internationally, the so-called “benchmark effect.” This paper finds that benchmark-driven investors indeed play a large role in a key segment of the market—the EM local currency government bond market—, accounting for more than one third of total foreign holdings as of end-2014. We find that the prominence of these investors declined somewhat after the May 2013 taper tantrum, but remain high. This distinction is important in understanding the drivers of EM capital flows and their sensitivity to different types of shocks. In particular, a high share of benchmark-driven investors may result in capital flows that are more sensitive to global shocks and less sensitive to country factors.

Do Investor Differences Impact Monetary Policy Spillovers to Emerging Markets?

We re-examine monetary policy spillovers to Emerging Market Economies (EME) in the form of capital flow reversals, using sectoral-level securities holdings data for Euro Area investors. In response to a surprise monetary tightening, active investors such as investment funds re-balance their portfolios away from EME, while more passive, long term investors such as insurance funds and banks exhibit no significant reaction on average. For active investors, the reallocation out of EME appears stronger under synchronized monetary tightening between the Fed and the ECB. However, these investors may even inject more capital to EME securities when the monetary tightening surprises contain positive news about the Euro Area economy. Issuers’ monetary-fiscal stability may explain the heterogeneous impact of these spillovers.

The Role of Different Institutional Investors in Asia-Pacific Bond Markets during the Taper Tantrum.

We examine the behaviour of different investors buying and selling emerging market government and corporate bonds around the 2013 taper tantrum. Using detailed security-level data on bond holdings by institutional investors from Thomson Reuters eMAXX, we find that mutual funds – which are subject to outflow pressures – tended to liquidate their bond holdings of emerging Asian bond markets, while insurance companies, annuities and pension funds – all of which are not subject to outflow pressures – bought extra bonds in these markets. We also find some evidence of global retrenchment during the taper tantrum. In particular, local (Asia domiciled) funds bought emerging Asian bonds, and global (US, UK and Europe domiciled) funds sold these bonds. These results suggest that policymakers need to foster a stable domestic investor base and make efforts to better understand the behaviour and incentives of different bond investors.

Chari, A, K.D. Stedman, and C. Lundblad (2021). Taper Tantrums: Quantitative Easing, Its Aftermath, and Emerging Market Capital Flows. The Review of Financial Studies, 34, 3, 1445ñ1508.

Chari, A, K.D. Stedman, and C. Lundblad (2022). Global Fund Flows and Emerging Market Tail Risk. NBER WP 27927.

Eichengreen, B., R. Hausmann and U. Panizza (2023) Yet it Endures: The Persistence of Original Sin. Open Economies Review, 34, 1-42.

Lee, A. (2022). Why Do Emerging Economies Borrow in Foreign Currency? The Role of Exchange Rate Risk. Working Paper.

Shek, J., I. Shim, and H.S. Shin (2018) Investor Redemptions and Fund Manager Sales of Emerging Market Bonds: How Are They Related? Review of Finance, 22 (1), 207ñ241.

Boermans, M.A., and J.D. Burger (2023). Fickle emerging market flows, stable euros, and the dollar risk factor. Journal of International Economics, 143, 103730.